As we nearly conclude the 3rd quarter of 2025, the property market shows some interesting changes.With this in mind, I wanted to share with you insights that you may find useful when considering moving, buying or selling in the market.

Zones 1 & 2 (£1M+ Market) – H1 2025 & July 2025 AnalysisThe first half of 2025 has demonstrated a measured yet active market in Prime Central and Inner London. Buyers are displaying heightened selectivity whilst maintaining genuine intent, though with a considerably sharper eye on value than previous years. This shift has prompted a necessary recalibration of seller expectations, creating a more balanced—albeit negotiation-heavy—marketplace.Market Recalibration: Pricing Adjustments Take HoldThe prime London property market is experiencing significant price recalibration as sellers align with current market sentiment. Asking prices for new listings declined by 6.4% year-on-year to £3.22 million from £3.4 million in the first half of 2024, whilst sales agreed prices fell by 3.6% to £2.46 million. This adjustment reflects sellers becoming increasingly realistic about buyer expectations in the current economic climate.Perhaps most telling is the discount between asking and achieved prices, which has widened to 23.5%—a substantial gap that underscores the negotiating power buyers currently wield. On a per square foot basis, sales agreed prices dropped 2.3% to £1,550, whilst new listings maintained asking prices at £1,953, further highlighting the pricing tension in the market.

Transaction Activity: Steady but SelectiveSales agreed volumes dropped to 1,091 in the first half of 2025, representing an 11.3% decrease from the same period in 2024 and sitting 4.9% below the six-year average. This decline suggests buyer caution at current price points, though the relatively modest 1.6% drop from H2 2024 indicates the market has found a degree of stability despite broader economic headwinds.The reduction in transaction volumes reflects a more discerning buyer base rather than a complete withdrawal from the market. Well-positioned, correctly priced properties continue to attract serious interest and competitive offers, whilst overpriced stock languishes.Supply Dynamics: More Choice, Strategic ListingsStock levels have climbed notably, with 13,756 properties available for sale in H1 2025 – up 4.3% from the previous year and 17% above the six-year first-half average. This increased inventory provides buyers with greater choice and negotiating leverage.Interestingly, new instructions dropped to 4,727, down 6.5% year-on-year, suggesting more strategic listing decisions from vendors. However, compared to the second half of 2024, listings surged by 25.9%, indicating renewed activity from sellers after a more subdued latter half of 2024.

Market Friction: Adjustments and NegotiationsThe market is experiencing increased friction as price expectations align. Price reductions climbed dramatically to 2,427—a significant 20.7% jump from H1 2024 and 45.7% above the long-term first-half average. This surge demonstrates sellers increasingly adjusting to meet buyer expectations rather than withdrawing from the market.Encouragingly, fall-throughs actually decreased by 11% to 258, remaining below average—a positive signal for deal progression once terms are agreed. Withdrawn listings stayed elevated at 3,474, only marginally down from last year, showing that some vendors prefer to wait rather than accept current market pricing.

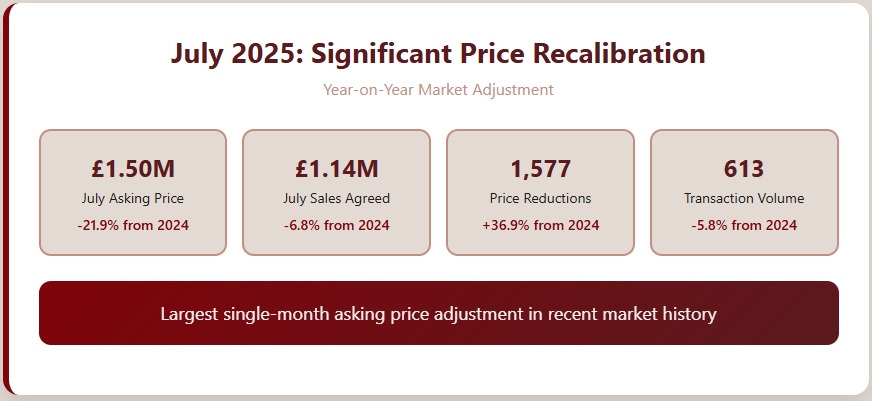

July 2025 Spotlight: Summer RecalibrationThe summer of 2025 finds the £1 million+ property market in a state of cautious recalibration. With interest rates stabilising after a volatile 24 months and political uncertainty softening post-election, July’s figures show a market beginning to find its rhythm—albeit with sellers and buyers often dancing to slightly different beats.Supply Remains ElevatedProperties for sale in July 2025 stood at 6,719, marginally higher than July 2024’s 6,680 and well above the six-year July average of 6,070. Supply levels remain elevated compared to pre-pandemic norms, suggesting sellers are testing the market—perhaps prompted by media coverage of a potential “buyer comeback” and desire to capitalise before any autumn slowdown.New listings rose modestly year-on-year to 1,755, up 3.2% from July 2024. However, this increase hasn’t translated to proportional buyer activity, with sales agreed dropping to 613—down 5.8% from the previous July and significantly below the 724 recorded in July 2022.

Dramatic Price AdjustmentsJuly witnessed the most significant pricing story of the year. Average asking prices for new listings plummeted 21.9% to £1,504,486 from £1.93 million in July 2024. This dramatic recalibration signals sellers are increasingly aware of buyer caution and affordability constraints, particularly in higher-value brackets.Sales agreed prices also declined to £1,141,240, down 6.8% year-on-year, though the reduction was less severe than asking price falls. This divergence suggests deals are still completing, but often after substantial negotiation.

Price Reductions SurgeSupporting the pricing narrative, price reductions hit 1,577 in July—up 37% compared to the previous July and well above the six-year average. This represents the most telling indicator of seller realism taking hold.Conversely, withdrawals fell to 1,174, slightly below the long-term average, hinting that once sellers adjust expectations, they’re more inclined to proceed. Fall-throughs remained steady at 180, closely aligned with historical norms.

Key Takeaways for Market ParticipantsFor SellersThe prime £1M+ market in Zones 1 & 2 remains highly active but increasingly selective. Success requires strategic pricing from the outset and exceptional presentation standards. The days of optimistic pricing strategies are firmly behind us—buyers clearly hold the advantage in current negotiations.Properties that are well-positioned, competitively priced, and move-in ready continue to attract multiple viewings and offers. However, vendors must be prepared for the negotiation process and potential price adjustments during marketing.For BuyersCurrent market conditions present opportunities for value-conscious purchasers willing to be decisive when the right property emerges. The increased stock levels provide greater choice, whilst the uptick in price reductions suggests room for negotiation on many properties.Buyers should focus on properties that have been realistically priced from launch or have undergone recent price adjustments, as these often represent the best value and most motivated vendors.Market OutlookWhilst transaction volumes remain below peak levels and values continue adjusting, the market appears to have found stability rather than continuing decline. The data suggests we’re witnessing a new era of negotiation-led transactions with more realistic pricing expectations on both sides.Agents employing clear pricing strategies and transparent communication will find opportunities in this evolving landscape. The market is no longer in freefall—it’s simply maturing into a more balanced, value-driven environment.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.

You can revoke your consent any time using the revoke consent button.

")