")

London Property Market Update 1Q22

With the 1st quarter of 2022 already complete, the London property market continues to experience lots of changes. Though the pandemic carries on, we are now seeing overseas buyers coming back to London. So here’s a summary of key elements of the market and indications of where things are heading for the rest of the year.

Average Property Price in London

Though London has really been struggling relative to the rest of the country during the pandemic and prior to that, Brexit, we’re finally starting to see some good momentum in terms of the property market which is reflected in the first-quarter results.

Property values in London have now hit a new high to an average of £534,977 according to lender Halifax. At the start of the first Covid lockdown in March 2020, the average London home cost £493,626 but prices have risen by £41,351 or 8.4% since then.

According to a different lender, Nationwide, the average property price in London is £518,333, representing a 7.4% increase since the start of the year. This represents a £58,000 increase since the start of the pandemic and is the fastest annual growth rate since 2016 when in the second quarter 2016, we saw prices increase on average by 9.9%.

How Does London Compare to the Rest of England?

London’s average annual rate of growth was 5.9% compared to a national average of 11% growth.

The average property price in the UK has reached a record of £282,753; rising by £43,000 during the pandemic.

Across the South-East, the market has been even stronger through the pandemic with prices going up £54,634 — or 16.5% — from £331,156 to £385,790.

What are the Key Factors Affecting the Property Market?

- Limited supply and strong demand. Despite the prospect of increasing pressure on households’ finances, people are still looking to buy.

- Stretching affordability. Data from the Financial Conduct Authority shows that increasing house prices are resulting in more buyers having to take out mortgages with a life of 35 years or more. In June 2021, 35,046 mortgages were sold with a term of at least 35 years, more than three times the level of June 2020.

- Higher savings. According to Nationwide’s chief economist, households accrued an extra £190 billion of deposits over and above the pre-pandemic trend since early 2020, due to the impact of Covid on spending patterns.

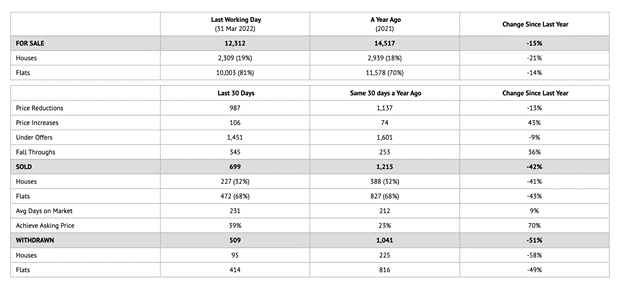

Greater London Inventory

In terms of transaction volume, the number of properties for sale in Greater London was 15% less than a year ago, with the houses component of that figure being down 21%.

As a result, we are seeing fewer price reductions with 987 of available properties having reduced their price versus 1,137 a year ago.

In Greater London, the average days on the market have also increased. As of 31 March 2022 the average days on the market was 231 days, an increase from 212 days a year ago. But, in comparison, the positive news for sellers is that 39% of the sold properties sold at asking prices versus only 23% a year ago.

London’s Luxury Market Highlights

In terms of Prime Central London and properties on the market of £1M or more, we are seeing them beginning to make a comeback as the world adjusts to life in a pandemic – with house prices up and discounts down.

Prices have risen particularly well in areas outside central London, such as Richmond, Wandsworth and Islington, as we see a ‘race for space’ brought on by the pandemic.

According to Coutts Bank, prices in Prime Central London are still down 7.8% from the peak in 2014. This has created an opportunity for those looking to buy centrally, as some areas are currently relatively cheap compared to historic levels.

For example, prices in Knightsbridge & Belgravia, some of the most prestigious area in London, are 17% below their peak in 2014. However, if you want to make the most of this, you will want to invest soon, as this downturn may be finally coming to an end as we are seeing greater demand from buyers both domestically and internationally.

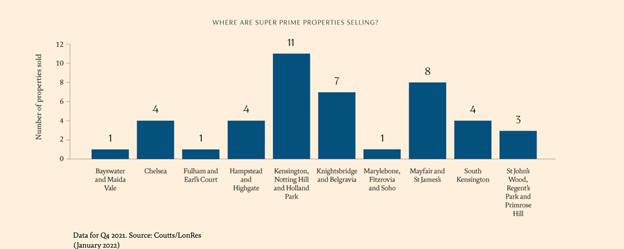

Super Prime Property Market Update

Meanwhile, the market for super-prime properties – those worth £10 million or more – has skyrocketed, with sales doubling in 2021 compared to the previous year, and October to December 2021 saw the highest number sold in any three-month period since 2016.

A few key findings around super-prime properties to note:

- The number of trophy homes sold in central London has returned to pre-pandemic levels, despite a lack of supply, the collapse of Russian-led deals and global instability.

- Sales volumes of multi-million-pound mansions were 33% higher this January than in the same month in 2019, and 31% higher last month than in February 2019, as the luxury central London market begins its recovery following the uncertainty of Brexit and the Covid-19 pandemic.

- New data published by LonRes shows that the spike in transactions has pushed up the average price tag of a property in the exclusive core of the capital by 5.9% compared to this time last year to £1,700 per square foot.

My Thoughts for the Coming Months

While stock is relatively low, and we are seeing increased demand, the market is still highly price sensitive so if you have a listing that’s not selling it’s really going to be impacted by the price. While there is a lack of inventory, buyers are still quite sensitive to making sure that they’re getting value for money.

London is still a safe haven in times of uncertainty, and I believe that this trend is going to continue. I am seeing US buyers coming back with an eagerness to have a diversified portfolio.

While nobody has a crystal ball on these things, overall speaking given the level of pent-up demand, we’re seeing a lot of activity right now, particularly in the higher end of the market.

If you would like to invest in the London property market, are thinking about buying a home, or selling your property to move on, I would love to help.

Please do reach out and we can arrange a consultation to discuss your needs and aspirations.